What It Takes to Be a Good Investor in Bitcoin (and Beyond)

Investing isn’t just about picking the right assets – it’s about cultivating the right mindset and habits. This is especially true in the world of Bitcoin, where wild price swings can test an investor’s resolve. Whether you’ve dabbled in stocks, real estate, or crypto and faced setbacks, don’t be discouraged. Becoming a successful investor is a journey of continuous learning and self-improvement.

In this article, we’ll explore the essential mindsets, philosophies, and habits that good investors share, with a focus on Bitcoin but plenty of real-world examples from other assets. We’ll also highlight common mistakes (we’ve all made them!) and how to avoid them.

Think Long-Term – Time in the Market vs. Timing the Market

One of the most important traits of a good investor is patience. Legendary investor Warren Buffett summed it up well: “The stock market is a device to transfer money from the impatient to the patient.” His point? Those who rush in and out of trades often lose to those who hold steady for the long run. This principle applies to Bitcoin just as much as to stocks or real estate.

Markets reward long-term thinking. Historical data backs this up. For example, since Bitcoin’s inception, simply holding it for a sufficient length of time has almost always led to profit. Glassnode data shows that out of 5,060 days of Bitcoin’s trading history, holding Bitcoin has been profitable on 4,954 days – that’s 97.9% of the time. In other words, if you bought Bitcoin on any random day in the past and held it to today, there’s a 97.9% chance you’d be up. This remarkable track record highlights Bitcoin’s consistent upward trajectory despite short-term volatility. It echoes a broader investing truth: given a fundamentally strong asset, time in the market is your ally.

Consider the stock market analogy. A J.P. Morgan study of the S&P 500 index from 1999–2018 found that an investor who stayed fully invested earned about a 5.6% annual return. But if they missed just the 10 best trading days, their return dropped to 2.0%, and missing the 20 best days turned their return negative. Missing the top 30 or 40 days was even more disastrous. The takeaway: a few big days often account for most of the gains, and you likely won’t catch those days if you’re jumping in and out. No wonder the old saying goes, “Time in the market is more important than timing the market.”

Real estate offers another great example. Property values generally increase over years and decades, not weeks. The most successful real estate investors take a long-term approach, aiming for sustainable growth through property appreciation and steady rental income. They understand that real estate (like other markets) moves in cycles, and they ride out slow periods or downturns by focusing on the long game.

So whether it’s Bitcoin, stocks, or property, think of investing as a marathon, not a sprint. Hopping around trying to time the peaks and valleys can leave you exhausted and empty-handed. Instead, set your sights years into the future. If you believe in the asset’s fundamentals, give your investment time to breathe and compound. As legendary trader Jesse Livermore famously noted (later echoed by Buffett’s partner Charlie Munger): “The big money is not in the buying and selling... but in the waiting.”

Do Your Homework – Understand What You Invest In

Ever bought into a stock or a coin because someone hyped it, only to later realize you had no clue what you actually owned? Don’t worry – many of us have been there. One hallmark of great investors is that they thoroughly understand their investments. This means doing your homework before you put your money in.

Warren Buffett followed a rule of never investing in businesses he doesn’t understand. During the dot-com bubble, he famously avoided hot tech stocks because they were outside his “circle of competence” – and that caution saved him from huge losses when the bubble burst. The lesson for us: know what you’re buying. In Buffett’s words, “If you aren’t willing to own a stock for ten years, don’t even think about owning it for ten minutes.”. He was talking about stocks, but the spirit applies to Bitcoin and crypto as well – if you don’t have a long-term belief in the asset, perhaps you shouldn’t buy it in the first place.

So, what does doing your homework entail? At a basic level, it’s researching and understanding the fundamentals:

For stocks: study the company’s business model, finances, industry trends, and competitive advantages. Ask, “Would I be comfortable owning this whole business, not just the stock ticker?” Good investors think like business owners, not gamblers.

For real estate: learn the local market, property values, rental rates, and expenses. Successful real estate investors often develop specialized knowledge in a niche (e.g. residential rentals in a certain city) and stick to what they know.

For Bitcoin and cryptocurrencies: understand the technology and value proposition. You don’t need to be a coder, but grasp the basics of why Bitcoin has value – for example, its fixed supply of 21 million coins (digital scarcity), its decentralized network secured by thousands of nodes, and its growing adoption as a store of value. Learn about key concepts like the Bitcoin halving cycle (which cuts new supply every four years) and how that has historically affected the price. In plain English: Bitcoin is often compared to “digital gold” because it’s hard money that doesn’t inflate easily – knowing that can strengthen your conviction during rough times. Also research any crypto you invest in: what problem does it solve, who is behind it, how widely is it used? If the answers are shaky or you can’t explain it to a friend, think twice before investing real money.

Doing your homework also means staying informed. Read reputable sources for news and analysis. For Bitcoin, sites like CoinDesk and Bitcoin Magazine provide on-chain data and insights. For instance, CoinDesk recently reported that as Bitcoin’s price rebounded in 2025, long-term holders were accumulating coins even as short-term traders sold – for every 1 BTC sold by short-term holders, long-term holders bought 1.38 BTC. This kind of information, gleaned from on-chain analytics, tells a story: seasoned Bitcoiners had strong conviction and were “buying the dip,” a signal of confidence. Understanding such trends can help you make informed decisions instead of reacting blindly to price moves.

Bottom line: Don’t invest because of hype or a hot tip alone. Invest because you’ve done the research and you truly believe in the asset’s long-term value. When you know why you own something, you’re far less likely to panic-sell it on a whim, and far more likely to hold or add when it’s undervalued. Knowledge builds conviction – and conviction is an investor’s best armor against uncertainty.

Plan – and Stick to It

A common trait among successful investors is that they have a plan. This doesn’t need to be a 50-page manifesto – it can be as simple as writing down your investment goals, time horizon, and strategy. The key is to set a strategy that makes sense for your situation and then stick to it through market ups and downs.

Why does having a plan matter so much? Because when markets turn turbulent (and crypto markets do), our emotions can lead us astray. If you’ve already defined a plan – say, “I’m investing $500 per month in Bitcoin and quality stocks for 10+ years” – you’re less likely to do something rash when prices swoon. Your plan reminds you of the big picture. Fidelity Investments puts it this way: creating a financial plan provides a foundation for investment success, and it’s important to stick to your plan even when markets look unfriendly. In practice, that means resisting the urge to abandon your long-term strategy because of short-term volatility.

Set clear goals for your investments. Are you investing for retirement in 20 years? For a down payment in 5 years? For your child’s education? Your goal will influence your strategy and what assets are appropriate. Bitcoin, for example, has delivered tremendous long-term gains, but it can be very volatile in the short term – if you need money for next month’s bills, that shouldn’t be in Bitcoin or stocks at all, but rather in a savings account or something safe. A good plan aligns your investments with your goals and risk tolerance.

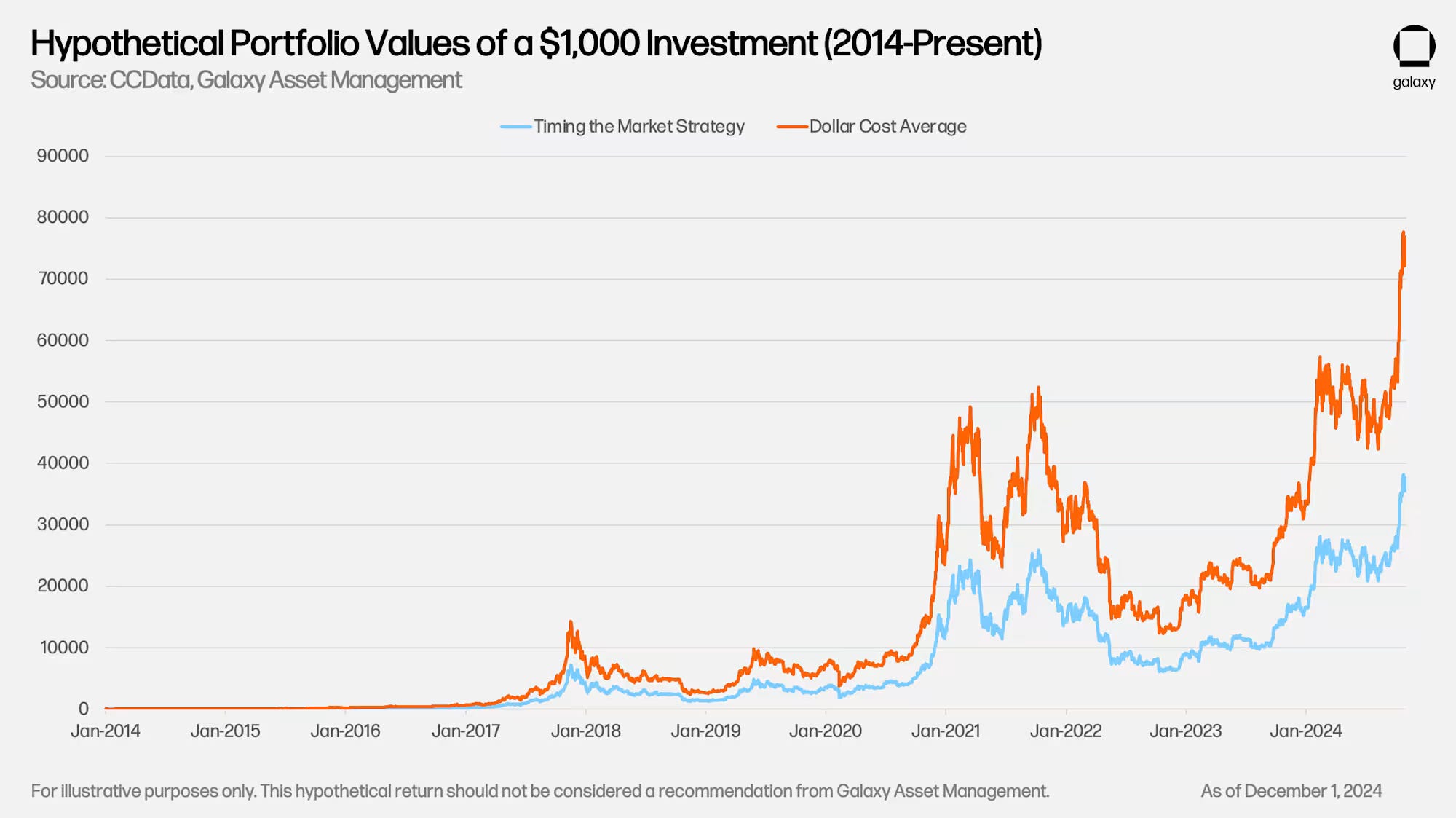

Part of planning is deciding how much to invest and how often. Many successful Bitcoin investors use a strategy called dollar-cost averaging (DCA) – investing a fixed amount at regular intervals (say weekly or monthly), regardless of price. This habit can take a lot of stress out of investing, because you’re not worrying about finding the “perfect” time to buy. Plus, it enforces discipline: you invest consistently, which harnesses the power of compounding. Fun fact: even an idealized strategy of trying to buy only dips was beaten by steady investing. A recent analysis found that simply investing consistently (DCA) into Bitcoin outperformed an almost impossibly perfect “buy the dip” strategy over the long run. The DCA approach delivered double the returns of a hypothetical trader who somehow timed every 20% dip perfectly (Timing the Market Strategy) – a scenario that in real life is nearly impossible! The message is clear: setting a regular investment plan and sticking to it usually beats fancy market-timing moves.

Your plan should also include what you’ll do when things get crazy (because at some point, they will). For instance, you might decide: “If Bitcoin or a stock doubles in value, I’ll sell 10% to lock in some gains, but keep the rest for the long term.” Or conversely, “If the price drops 50% but nothing fundamental has changed, I’ll take it as an opportunity to buy more at a discount.” These are examples of rules you might set for yourself so that you’re not making spur-of-the-moment decisions driven by fear or greed. As Buffett advises, “Be fearful when others are greedy, and be greedy only when others are fearful.” Having a plan that includes predetermined actions can help you actually follow that wise contrarian advice when the time comes.

Manage Risk: Diversification and Safety Nets

All investing involves risk. Good investors respect the risks instead of ignoring them. Two key practices help manage risk: diversification and having a safety net (or as Buffett might say, an “emergency fund”).

Diversification is a fancy term for not putting all your eggs in one basket. Markets can be unpredictable – even the best-looking bet can falter – so it’s wise to spread your investments across different assets. Fidelity calls diversification one of the foundations of successful investing because owning a variety of assets can help control risk. A well-diversified portfolio might include a mix of stocks across industries, bonds, real estate, and perhaps some Bitcoin or other crypto (depending on your interest and risk tolerance). The idea is that when one asset zigs, another zags – so you’re not overly exposed to a single point of failure. No single investment should be able to ruin you.

In the context of crypto, diversification can mean not going all-in on one coin or one type of token. Bitcoin itself is considered by many as the “blue chip” of crypto – it’s the oldest, most decentralized, with the largest market capitalization. Some crypto investors choose to hold mostly Bitcoin with a smaller portion in other established projects (like Ethereum), to balance potential high rewards with lower risk. Others prefer to diversify across asset classes: for example, you might allocate, say, 60% stocks, 20% real estate (REITs or properties), 10% Bitcoin, 10% cash or bonds. The exact numbers depend on your situation, but the principle is to avoid concentration risk. Even billionaire real estate moguls follow this rule – as one real estate investment guide notes, the best investors “do not place all their eggs in the same basket” and often invest beyond real estate, in stocks or bonds, to build a more resilient overall strategy.

Another aspect of risk management is not over-leveraging (i.e., not borrowing too much to invest). Leverage can amplify gains and losses. Many folks learned this the hard way during the 2008 housing crash – people took on mortgages they couldn’t afford, betting home prices would always rise. When the opposite happened, highly leveraged investors were wiped out. Similarly, in crypto, using margin (borrowed funds) to trade can be very dangerous given how volatile these assets are. A good investor knows to only take on risk they can survive. A simple rule: Never invest money you can’t afford to lose. Bitcoin can drop 50% or more in a matter of months (it’s happened multiple times). If losing that money would break you, you’ve invested too much.

Speaking of survival, maintaining a safety net of cash or liquid, safe assets is a hugely underrated habit. Buffett’s company Berkshire Hathaway famously holds tens of billions in cash or cash-equivalents at any time. Why? It provides security during downturns and lets him pounce on opportunities when others are forced to sell. In 2008, because Buffett had cash, he was able to inject money into Goldman Sachs on favorable terms when everyone else was panicking. For an individual investor, a safety net means having an emergency fund (e.g. 3-6 months of living expenses in cash) so that if you lose your job or face a medical bill, you don’t have to liquidate your investments at a bad time. It also means you won’t be a forced seller in a crash – often, having just a bit of cash reserve can prevent selling stocks or Bitcoin at rock-bottom prices out of sheer need. This aligns with Buffett’s advice to never be in a position where you must sell: keep enough cash so you can ride out storms.

Finally, consider setting some rules or tools to limit downside. For example, some stock investors use stop-loss orders (automatically selling if a price falls to a certain point) to cap their losses. Crypto markets are 24/7 and notoriously swingy, so if you’re trading actively, that could be useful. However, if you’re a long-term investor, you might instead set mental stop-losses or thresholds for re-evaluating an investment (since automatic sells in a flash crash might boot you out at the worst time).

Another risk management tactic is position sizing – don’t make any single investment position so large that its loss would devastate your portfolio. If Bitcoin is 50% of your portfolio, you must be prepared (mentally and financially) for the possibility it could drop drastically. Some very successful crypto believers keep a high percentage in Bitcoin, but they do so because they have conviction and they can afford the risk. Always measure risk against your own capacity.

In summary, spread your bets, don’t bet the farm, and keep some cash in reserve. These habits won’t eliminate risk (nothing can), but they dramatically increase your ability to weather the unexpected and stay in the game for the long term.

Master Your Emotions: The Psychology of Investing

If there’s one factor that separates good investors from mediocre ones, it’s often temperament, not IQ. As humans, we’re wired with emotions that served us well in hunter-gatherer days but often betray us in markets. Fear and greed are the classic culprits. Learning to manage these emotions – to be emotionally disciplined – can prevent costly mistakes.

Let’s talk about fear first. Picture this: Bitcoin’s price has plummeted 50% in a month. The news is full of doom and gloom, your portfolio value has shrunk, and your stomach is in knots. A natural response is fear – “I need to get out now before I lose more!” Many investors have sold in such panic moments, only to see the market stabilize and recover soon after. This cycle has repeated through history. For example, those who sold stocks in March 2020 during the COVID crash missed one of the fastest rebounds ever. Those who panic-sold Bitcoin in past crashes (like the 2018 crypto winter) often did so at the worst possible time – right near the bottom – crystallizing huge losses. Panic selling is often a mistake born from short-term fear. The antidote is to zoom out and remember why you invested and that downturns are usually temporary. If the fundamentals remain intact, patience tends to pay off. As one Bitcoin analyst noted, “corrections are normal in crypto. Expect them, plan for them, and don’t panic when they arrive.”

To manage fear, it can help to tune out constant price watching. If you’re holding for years, checking the price every hour will just toy with your emotions. Some of the steadiest Bitcoin holders will tell you they don’t even look during crashes. Instead, they focus on long-term metrics (like the growing number of users or improvements in the technology) which give confidence that the value will recover. And history shows Bitcoin has always recovered from its drawdowns to reach new highs eventually, as long as you gave it enough time. For instance, Bitcoin plunged over 80% from its 2017 peak (near $20,000) to a low around $3,200 at the end of 2018. That crash shook out a lot of newcomers. But those who held on through the “despair” of 2018 were vindicated – by late 2020, Bitcoin was back above $20k, and in 2021 it soared to $69k, far surpassing the previous peak. The cycle repeated: an even bigger crash in 2022 (down ~75% from the 2021 high) was followed by recovery in 2023–2025. The pattern is that the weak hands who panic sell in the bust end up effectively transferring their coins to the strong hands who hold or buy during the bust. Or as Buffett would say, money goes from the impatient to the patient.

Now, greed is the flip side. This kicks in when markets are up and everyone is making money. It’s the “maybe I should double down, borrow money, take even bigger risks – I can’t lose!” feeling. Greed makes people ignore risk and chase ridiculous returns. In the crypto realm, this might manifest as pouring money into the latest meme coin because it’s gone up 1000% in a week (never mind that it has zero fundamental value), or using high leverage to try to multiply gains. Greed had people mortgaging their homes to buy Bitcoin at $19k in December 2017 – sadly, many of them were wiped out in the crash that followed. Greed also fueled the ICO mania in 2017 and the DeFi yield craze in 2020, where inexperienced investors jumped into anything that promised huge returns, only to lose most of it when the bubble popped. The lesson: when you catch yourself feeling invincible or when everyone around you is bragging about easy money, that’s a sign to take a step back and be cautious. As Buffett famously quipped, “Be fearful when others are greedy.” This doesn’t mean you should never ride a bull market – by all means, enjoy the good times – but stay grounded. Keep evaluating the real value of what you own relative to its price. If an asset’s price has gone way beyond what reason and data can justify, be willing to trim your position or at least refrain from adding more. Protect your gains.

A useful habit here is to pre-commit to certain actions when you are in a cool, rational state (as part of your plan). For example, you might decide: “If my crypto portfolio doubles, I will sell 20% and rebalance into safer assets.” That way, when euphoria is running high, you have a rule to counteract the greedy impulse to just let it all ride. Conversely, you might commit: “If the market crashes by 50%, I won’t sell in panic; instead I might even allocate fresh savings to buy while it’s cheap.” By having these rules, you don’t leave yourself at the mercy of emotions in the heat of the moment.

Finally, cultivate a bit of contrarian thinking. Not in a reflexive “always do opposite of the crowd” way (the crowd is right sometimes), but in the sense of independent thinking. Don’t simply follow the herd. Often the herd buys high and sells low – the opposite of what you want. For instance, a lot of retail investors only wanted Bitcoin when it was nearing $60k+ in 2021 (greed), but wanted nothing to do with it at $16k in late 2022 (fear) – whereas a good investor would do the reverse: lighten up near euphoric peaks and accumulate in the depressed troughs. It takes emotional fortitude to do that! One trick is to invert the scenario: ask “How will I feel if I sell now and it rebounds tomorrow? How will I feel if I hold and it drops further?” Try to avoid the action that you know you’re only taking out of sheer fear or greed.

To sum up this section: recognize your emotional triggers. You can’t eliminate feelings (and you shouldn’t try to be a robot), but you can train yourself to respond calmly. Keep a cool head when others are losing theirs. If you can do that, you’ll already be ahead of most investors.

Cultivate Good Habits and Continuous Learning

Being a good investor is a bit like staying physically fit – it’s not a one-time accomplishment, but an ongoing process of maintaining good habits. The great news is that anyone can develop these habits. Here are a few to focus on:

Continuous Learning: The best investors are always learning. They read books, annual shareholder letters, research reports, and credible websites. If you’re into Bitcoin, read articles from sources like Bitcoin Magazine or CoinDesk, follow reputable analysts on Twitter (X) or newsletters, and consider reading foundational texts (for example, The Bitcoin Standard by Saifedean Ammous for understanding Bitcoin’s economic thesis). For stocks, classic books like Benjamin Graham’s The Intelligent Investor or Peter Lynch’s One Up on Wall Street are gold mines of wisdom. The point isn’t to copy someone else’s style, but to absorb lessons from history and experienced players. Markets evolve, so keep an open mind and a student mentality. Even legendary investors like Buffett in his 90s still say they learn every day.

Stay Informed (but Avoid Noise): There’s a fine balance between staying reasonably up-to-date versus being glued to every tick or sensational headline. Successful investors follow the right indicators. For Bitcoin, that could be on-chain metrics (like how many long-term holders exist, or the mining hash rate) rather than the latest rumor on Reddit. For stocks, that might be quarterly earnings and economic trends rather than daily CNBC chatter. Figure out what information truly matters to your investments and focus on that, filtering out the rest. And remember: the news tends to be emotionally charged. Try to read it with a skeptical, analytical eye rather than getting swept up.

Regular Review and Reflection: Good investors periodically review their portfolio and strategy. This isn’t about knee-jerk changes, but rather checking if your allocations still align with your goals and risk tolerance. Maybe Bitcoin grew to be a larger chunk of your portfolio than you intended after a big price increase – you might rebalance by trimming some profit. Or maybe your life situation changed (say, you have a child now), and you want to be slightly more conservative. Adjust thoughtfully. Also, reflect on your past decisions. Every investor makes mistakes – the key is to learn from them. Did you panic sell something and later regret it? Next time you can remind yourself of that regret when you feel the urge to panic. Did you chase a speculative tip that went bust? Next time you’ll remember to do your research. Keep a journal or mental notes of what you’ve done right and wrong.

Automation and Discipline: Where possible, automate good behaviors. For instance, you can set up an automatic monthly transfer from your paycheck to an investment account or crypto exchange. This “pay yourself first” approach ensures you consistently invest before you get the chance to spend that money. It also turns investing into a routine, rather than something you do only when you feel like it. Many people find that treating investments like a “subscription” (to their future self) is effective. Automation leverages our laziness for good – if it’s automatic, you’re less likely to sabotage it. Of course, still review periodically, but try not to tinker unnecessarily.

Community and Mentorship: This one is often overlooked. Investing can be solitary, but you can benefit from engaging with a community of like-minded, level-headed investors. That could be a local investment club, an online forum (with caveats – many online spaces are full of noise; seek out high-signal communities), or just a few friends who are knowledgeable and rational. Discussing ideas helps you learn and stay motivated. Just be cautious to think for yourself at the end of the day – don’t follow someone blindly – but do leverage collective wisdom. In the realm of real estate, for example, many investors credit mentors or networking for their success. In crypto, finding trustworthy educators (like some well-respected podcast hosts or analysts) can rapidly deepen your understanding.

Lifestyle Habits: Believe it or not, general lifestyle can impact your investing. Being healthy, getting enough sleep, and managing stress can keep your mind sharp and less prone to emotional swings. If you’re trading actively, this is especially true – fatigue and stress lead to mistakes. Even if you’re long-term investing, a clear mind will help you stick to your strategy during trying times.

One more habit to cultivate is optimism balanced with realism. Great investors are often optimistic – you need optimism to believe that the assets you invest in will grow in value over time. Optimism about the future is what fuels investment in the first place. However, they pair it with a grounded realism about risks and human behavior. For example, you might be optimistic that Bitcoin’s adoption will continue to increase globally (indeed, an estimated 560 million people worldwide owned crypto by 2024, a number that has been steadily growing), but you remain realistic that the journey will be volatile and there will be crashes along the way. This balanced outlook helps you stay the course without being naïve.

Avoiding Common Mistakes: What Not to Do

We’ve touched on many of these throughout, but it’s worth explicitly summarizing some common investing mistakes that trip up both beginners and experienced folks alike. Awareness is the first step to prevention. Here are some frequent pitfalls and how to avoid them:

Chasing the Hype (FOMO): Jumping into an investment solely because it’s going up and everyone is talking about it. Example: buying a coin or stock at its peak price because it’s “hot.” Avoid this by doing your own analysis and questioning the hype. If everyone says “it can only go up,” be skeptical. Remember the dot-com mania or various crypto manias – what goes straight up can come straight down.

Panic Selling in Downturns: We discussed this – selling out of fear during a crash locks in losses. Avoid by zooming out and sticking to your plan. Only sell if the fundamentals are truly damaged, not just because price fell. Often the best opportunities come when you’re most scared (and others are panic selling).

Overtrading: Constantly buying and selling, trying to time every wiggle. This racks up fees, taxes, and mental stress, and typically underperforms a simple buy-and-hold strategy. Avoid by being patient and only making moves when you have a solid reason (not out of boredom or impulse). As an example, studies have shown even professional traders often can’t beat the market after fees – for most of us, less trading = more wealth.

Lack of Research: Investing in things you don’t understand because someone else said it’s good. This can lead to nasty surprises. The antidote is DYOR – Do Your Own Research – as we highlighted. If you don’t have time to understand an investment, consider not investing in it at all.

No Diversification (All Eggs in One Basket): Betting everything on one stock or one crypto hoping to hit the jackpot. Some people get lucky doing this, but many others blow up. It’s like driving without a seatbelt – maybe you’ll never crash, but if you do, the outcome is tragic. Avoid by diversifying across a few different investments. If one investment going to zero would ruin you, you’re overexposed to it.

Overleverage (Borrowing Too Much): Using debt or margin to invest more than you safely should. This can amplify gains for a while, but if the market moves against you, it can wipe you out completely (and even leave you owing money). In crypto, countless traders have been liquidated (had their positions forcibly sold) because they used high leverage and a price dip blew through their collateral. Avoid by using little or no leverage, especially in volatile assets. If you do use borrowing (like a mortgage for a house, which is quite common), ensure you can handle the payments and have a buffer for downturns. As a rule, never borrow to invest in something as volatile as crypto – that’s asking for trouble.

Ignoring Security Basics (for Crypto): This is specific to digital assets – mistakes like leaving all your coins on an exchange that gets hacked or not safeguarding your wallet keys. A tragic example is people who lost Bitcoin because they forgot or misplaced their private keys (passwords) – there’s no helpline to recover those. Avoid this by learning basic crypto security: use hardware wallets or reputable platforms, enable two-factor authentication, keep backups of your keys/passwords in a secure place, and never share your seed phrase. Treat crypto like cash or jewelry – protect it from thieves and accidents.

Falling for Scams: Unfortunately, the investing world (and especially crypto) has scams. If something promises “guaranteed” high returns with no risk, it’s likely a scam. Ponzi schemes and fake “too-good-to-be-true” opportunities abound. Avoid by being skeptical of any scheme that isn’t transparent and regulated. Stick to known investments and if you venture into new areas, double-check legitimacy (e.g. is that new crypto project audited? Who is behind it?).

Not Having an Exit Strategy: Some investors never think about how or when they’ll take profits or cut losses. They ride an investment all the way up…and all the way back down. While we advocate long-term thinking, it’s also wise to periodically realize gains or rebalance. Avoid the mistake of round-tripping your profits by deciding ahead of time under what conditions you’ll sell or trim a position. It could be based on valuation (e.g., “if my stock’s P/E ratio gets absurdly high, I’ll take some profit”) or life needs (e.g., “when this investment reaches my goal of $X, I’ll use some of it to pay off debt or buy a house”). On the flip side, know when to cut a loss if the thesis is broken – don’t hold a failing investment out of pure hope.

Following the Crowd Blindly: This is a general one – just because “everyone” on social media is buying something doesn’t mean it’s wise. By the time a trend becomes obvious, it might be near its end. Avoid herd mentality by keeping your independent judgment. It’s fine to take note of popular trends (sometimes the crowd is right for a while), but always ask if it truly fits your strategy and if you’re not just being swept up by crowd psychology.

If you recognized your own past behavior in any of these mistakes, don’t feel bad – every investor, even the greats, has made mistakes. The goal is not to be perfect, but to learn and not repeat the big mistakes. Success in investing often comes from avoiding the big blunders (like going all-in on a fad or panic selling at the bottom) and doing the simple things right (like staying invested, diversified, and patient).

Real-World Examples & Legendary Lessons

Sometimes the best way to internalize these principles is through stories of those who’ve done it right (and wrong). Let’s look at a few notable investors and scenarios for inspiration and caution:

Warren Buffett (Stocks): We’ve cited Buffett a lot because his wisdom is evergreen. He became one of the richest people by consistently applying sound principles: investing in businesses he understands, holding for the long term, and keeping a calm temperament. He held onto stocks through crashes and was ready to buy when others were fearful. Notably, Buffett’s wealth snowballed later in life – a huge chunk of it came after he turned 50 – highlighting the power of compounding given time. Also, Buffett’s discipline in minimizing costs and not overtrading (he famously said his favorite holding period is “forever”) shows the benefit of low friction and patience. However, even Buffett isn’t infallible; he admits to mistakes (like not buying certain great tech companies earlier). The lesson is the overall strategy and mindset matters more than any single decision.

The Bitcoin Early Adopters: Consider someone like Hal Finney or other early Bitcoiners who acquired BTC when it was under $100 and held on for years. They endured gut-wrenching volatility – 80% crashes were not theoretical, they were lived experiences – yet their belief in Bitcoin’s fundamentals kept them invested. By not selling early, they reaped exponential returns as Bitcoin gained global traction. An anecdote often told is that of Laszlo Hanyecz, who spent 10,000 BTC on two pizzas in 2010 (worth over $300 million at 2025 prices!). It’s a fun bit of lore but also a caution: even believers might wildly underestimate how an asset can appreciate long-term. While taking some profits is sensible, don’t sell all your investment just because it doubled or tripled – if the long-term story is still intact, the biggest gains might be yet to come. Many people sold Bitcoin at $1, $10, $100, thinking “that’s it, it can’t possibly go higher” – the visionaries who held on through multiple cycles became the stuff of legend (and very wealthy).

Dot-Com Bust Survivors: In the early 2000s, tech stocks crashed brutally. Amazon.com, for example, lost over 95% of its value when the dot-com bubble burst. A share of Amazon went from the equivalent of $113 in late 1999 to under $6 by 2001 – a lot of investors gave up on it. But those who had done their research on Amazon’s business and kept faith in its long-term potential (or even bought more at the lows) were handsomely rewarded: fast forward and Amazon became an e-commerce titan worth trillions, with its stock price thousands of percent higher than the 2001 lows. The key insight is that temporary crashes didn’t matter if the company (or asset) eventually fulfilled its promise. This parallels Bitcoin – it’s a high-growth, disruptive technology that has seen massive drawdowns, but each time it reached new highs later. The caveat: not every dot-com stock recovered (many died), just like not every altcoin will survive today. This underscores why understanding fundamentals is crucial – Amazon had real growing business behind the scenes, which is why it rebounded. Make sure what you invest in has true substance to justify long-term confidence.

Real Estate Patience: Think of a real estate example like someone who bought property in a prime location decades ago. Over time, rents increased, the neighborhood developed, and property values rose dramatically. They might have lived through interest rate spikes or housing recessions where prices stagnated for years, but ultimately, by holding for the long term, they built substantial wealth. A case in point: Many families who simply held onto homes in expensive cities (like New York, London, or San Francisco) for 30-40 years found those homes worth many multiples of the purchase price. On the other hand, speculative flippers who over-leveraged in 2006-2007 got caught in the 2008 crash and lost homes to foreclosure. The contrasting outcomes teach us about conservative long-term investing vs. short-term speculative gambling. Real estate investors often say “time in the market beats timing the market”, just like with stocks – it’s the same principle wearing different clothes.

Michael Saylor and MicroStrategy (Bitcoin Treasuries): A more recent Bitcoin-specific example is Michael Saylor, the CEO of MicroStrategy, who in 2020 started converting a large portion of his company’s treasury into Bitcoin as a long-term store of value. He faced skepticism and watched Bitcoin go through a severe bear market in 2022. But he publicly remained steadfast in his conviction, even buying more during dips. By 2025, as Bitcoin’s price reached new highs, MicroStrategy’s bold strategy appeared vindicated with multi-billion dollar gains on their BTC holdings. Saylor’s approach highlights conviction and sticking to a thesis – though it’s an aggressive strategy not suitable for everyone (definitely an example of concentrated risk/reward). It also shows how institutional adoption (companies and funds buying Bitcoin) has become a driving force – something early retail investors bet on long ago that is now coming true.

Lessons from Mistakes: It’s also valuable to recall stories of famous blunders. For instance, many investors in the 17th-century Tulip Mania or the more modern meme stock frenzy of 2021 got caught up in a frenzy over assets with little intrinsic value. When reality set in, prices collapsed, and fortunes were lost. The mistake? Speculating with no regard to value or risk, purely hoping to sell to someone else at a higher price (the “greater fool theory”). Avoid being left holding the bag by always asking: “Am I investing, or just speculating that someone will pay more later without any fundamental reason?” If it’s the latter, tread carefully or not at all.

Each of these examples reinforces a key idea we’ve discussed: patience, knowledge, discipline, and risk management pay off, while hype-chasing, fear-driven selling, and ignorance lead to regret. Keep these stories in mind when you face your own tests in the market. They can be a guiding light – if others got through similar challenges by sticking to sound principles, so can you.

Conclusion: Becoming a Better Investor

By now, you’ve seen that being a good investor isn’t about having a crystal ball or a genius IQ. It’s about mindset and habits that anyone can develop:

Patience and long-term vision to allow your investments to grow.

Thorough research and understanding to build true conviction.

A solid plan and consistent strategy, rather than ad-hoc decisions.

Risk management through diversification and not overextending, so you can survive the bad times.

Emotional discipline to resist the urges of fear and greed that derail so many.

Continuous learning and self-improvement, because markets evolve and so must we.

And of course, learning from mistakes, not repeating them.

The encouraging news is that even if you’ve struggled in the past (lost money, made rash moves, etc.), you can absolutely improve. Many of today’s seasoned investors have war stories of early blunders. What sets the successful apart is they didn’t give up – they reflected, adjusted, and tried again with more wisdom. You can do the same. If you treat each setback as tuition in the school of investing, you’ll come out smarter and stronger.

Investing, especially in something as revolutionary as Bitcoin, can be incredibly rewarding. It can also be nerve-racking at times. Embrace the journey – the ups and the downs. When the next volatility wave hits, remember that this is par for the course. If you’ve positioned yourself well (both financially and mentally), you can ride it instead of being wiped out by it. And when the next bull run has everyone euphoric, stay humble and stick to your principles, taking a page from the greats who have seen cycles come and go.

In closing, think of investing like tending a garden. You prepare the soil (education and planning), plant good seeds (sound investments), water and nurture regularly (adding savings, rebalancing, monitoring), and patiently wait for the fruits to grow. You can’t force a plant to grow faster by tugging on it; likewise, you can’t force quick riches without taking irresponsible risks. But given time, that garden can flourish and feed you abundantly. Keep cultivating those good investor habits, and over time you’ll likely be amazed at how much you grow – both in wealth and in wisdom.