Is Dollar-Cost Averaging Effective for Bitcoin Accumulation?

Dollar‑cost averaging (DCA) is an investment strategy where you buy a fixed dollar amount of an asset at regular intervals, regardless of its price. For volatile assets like Bitcoin, DCA is often recommended to “take the guesswork out of timing the market”. Instead of investing a lump sum all at once, DCA “averages out the cost of purchases” over time. Proponents argue this can reduce the impact of market swings – for example, buying more Bitcoin when prices dip and less when prices rise. However, detractors note that in a generally rising market (like recent years for Bitcoin) a lump‑sum investment can accumulate more Bitcoin over time. The question of effectiveness depends on one’s goals and risk tolerance. Below we examine pros and cons of DCA for Bitcoin and summarize relevant data and studies.

What Is DCA and Why Use It?

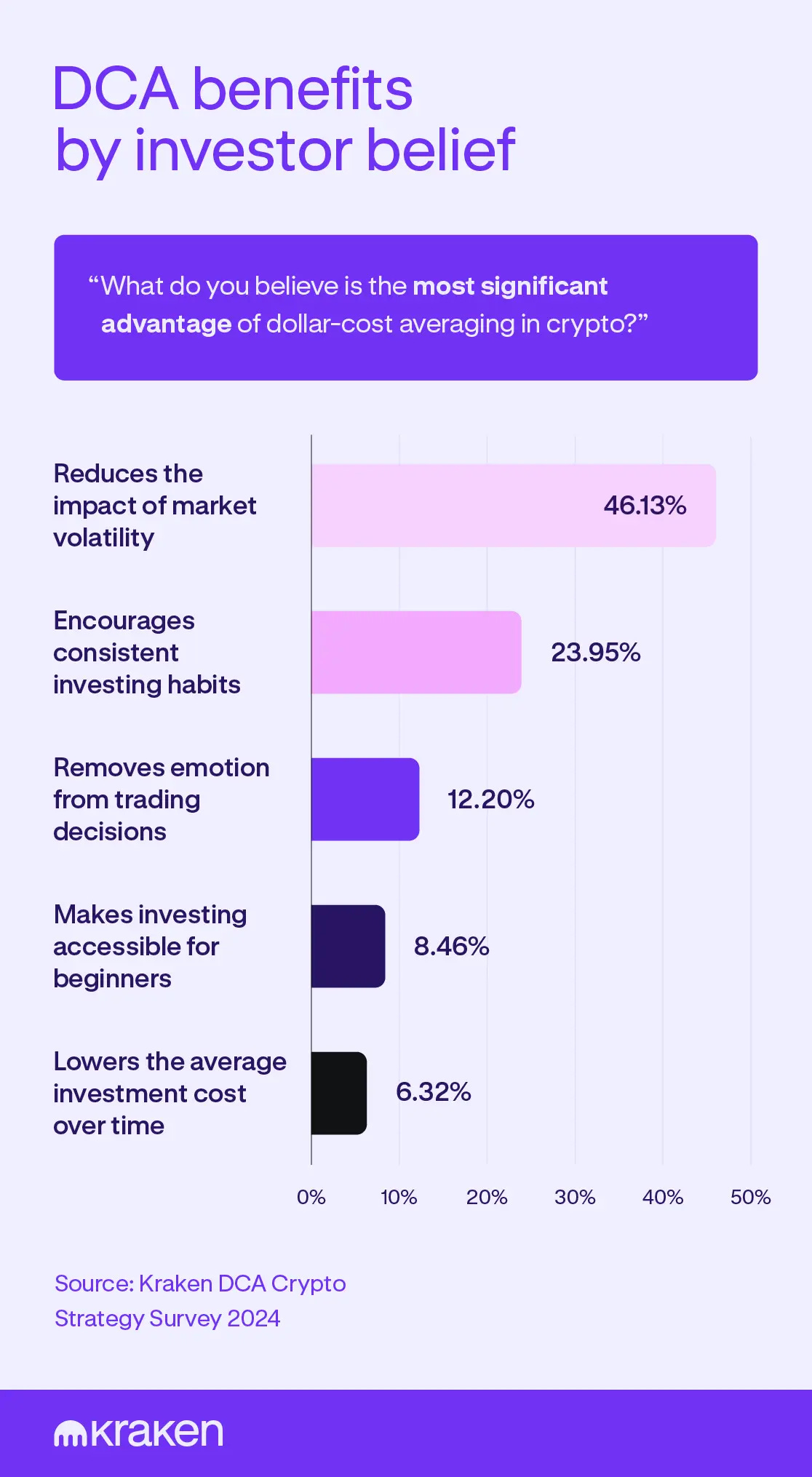

DCA means investing the same amount on a regular schedule (e.g. $100 every week or month) instead of a one‑time purchase. For instance, one might buy $100 of Bitcoin on the 1st of every month. As Kraken explains, DCA “allows investors to buy more of an asset when prices are low and less when prices are high, effectively averaging the cost over time”. Coinbase notes it’s especially appealing when an investor believes an asset will appreciate in the long run but is unsure about short‑term volatility. By continuously investing regardless of market direction, DCA helps avoid mistiming a single large purchase. In crypto, many exchanges offer automated recurring buys for this reason – a 2024 Kraken survey found 83% of crypto investors have used DCA and 59% call it their primary strategy.

Pros of DCA for Bitcoin

Mitigates timing risk and emotion. DCA smooths out purchases over time, so you aren’t trying to “buy the bottom.” As Coinbase notes, it’s a way to “own crypto without the notoriously difficult work of timing the market”. Fidelity similarly points out DCA “helps take some of the guesswork and emotions out of entering the market”. By following a schedule, investors avoid panic‑buying at peaks or missing dips.

Reduces impact of volatility. Bitcoin is famously volatile: for example, it fell under $20,000 in late 2022 then surged to record highs above $100,000 by late 2024. DCA spreads your buys across these swings. In practice, that means each dip lets you accumulate more Bitcoin for your money, potentially lowering your average cost. Over a long bull run, buying more on dips can slightly improve returns compared to a single purchase just before a peak.

Builds investment discipline and is beginner-friendly. DCA encourages consistent saving and investing habits. It’s often easier for new or cautious investors to commit small amounts regularly than a large lump sum. As the Kraken Learn team notes, DCA is a “hands-off strategy” for steadily growing holdings without constant market watching. This low‑stress approach can make Bitcoin accumulation more accessible, especially when prices seem daunting.

Strong historical gains. Despite market ups and downs, Bitcoin’s long-term trend has been upward. For example, a 2024 analysis showed that a $10 weekly DCA from mid-2019 to mid-2024 would have turned $2,620 into $7,913 – a 202% return. By contrast, the same $10 per week in gold only grew ~34% in that period. This highlights that even regular small buys in Bitcoin have historically yielded very high gains over multiple years. (Of course, past performance does not guarantee future results.)

Source: coinbase.com

Cons of DCA for Bitcoin

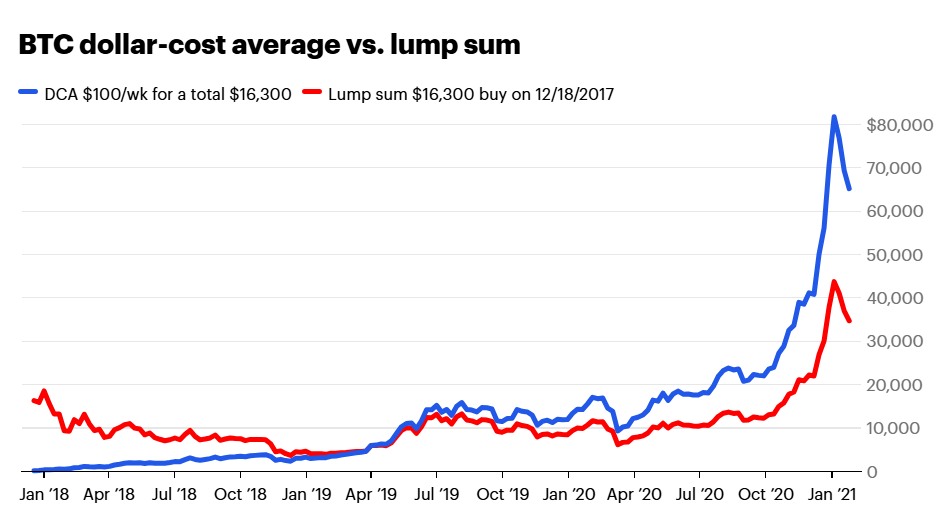

Potentially lower returns vs. lump-sum. If Bitcoin’s price generally rises over your investment horizon, putting money in all at once often earns a higher return. Fidelity notes that “a lump‑sum investment is likely to do better” when prices go up over time. In fact, a detailed backtest found that, on average, a 12-month DCA plan accumulated 75% less Bitcoin than investing the whole amount immediately. Even a 6-month DCA plan held ~25% less. In other words, DCA can leave more money on the sidelines (in cash) which then misses out on Bitcoin’s climbs.

Missed upside in strong bull markets. Relatedly, during fast rallies a lump-sum buy at the beginning would capture more of the run‑up. One analysis points out that DCA’s “limit (missed profit) in an upward moving market” is a drawback. For example, had someone bought $100 in Bitcoin in January 2023 ($16,500) as a lump sum, they would have realized huge gains by late 2024. A DCA buyer putting $8.33 weekly ($100/month) over the same year would have spent more at higher prices later, getting fewer total coins.

Fees and carrying cash. Dollar‑cost averaging means making many transactions. Each buy can incur fees (trading fees, or bid-ask spreads) which can eat into returns, especially for small periodic purchases. In addition, DCA requires keeping cash on hand between purchases. If interest rates on that cash are low, the unused portion effectively loses some purchasing power. (This cost is negligible if you’re investing directly from each paycheck, but it matters if saving up a lump sum to invest slowly.)

Does not eliminate risk. Bitcoin can fall for years. DCA will continue to buy as scheduled even when prices are dropping, but it doesn’t prevent losses. Over a prolonged bear market, your portfolio value can still go down (though you will at least keep acquiring cheaper coins). DCA only spreads risk – it can’t guarantee profit or protect against a collapsing market.

Historical Context and Studies

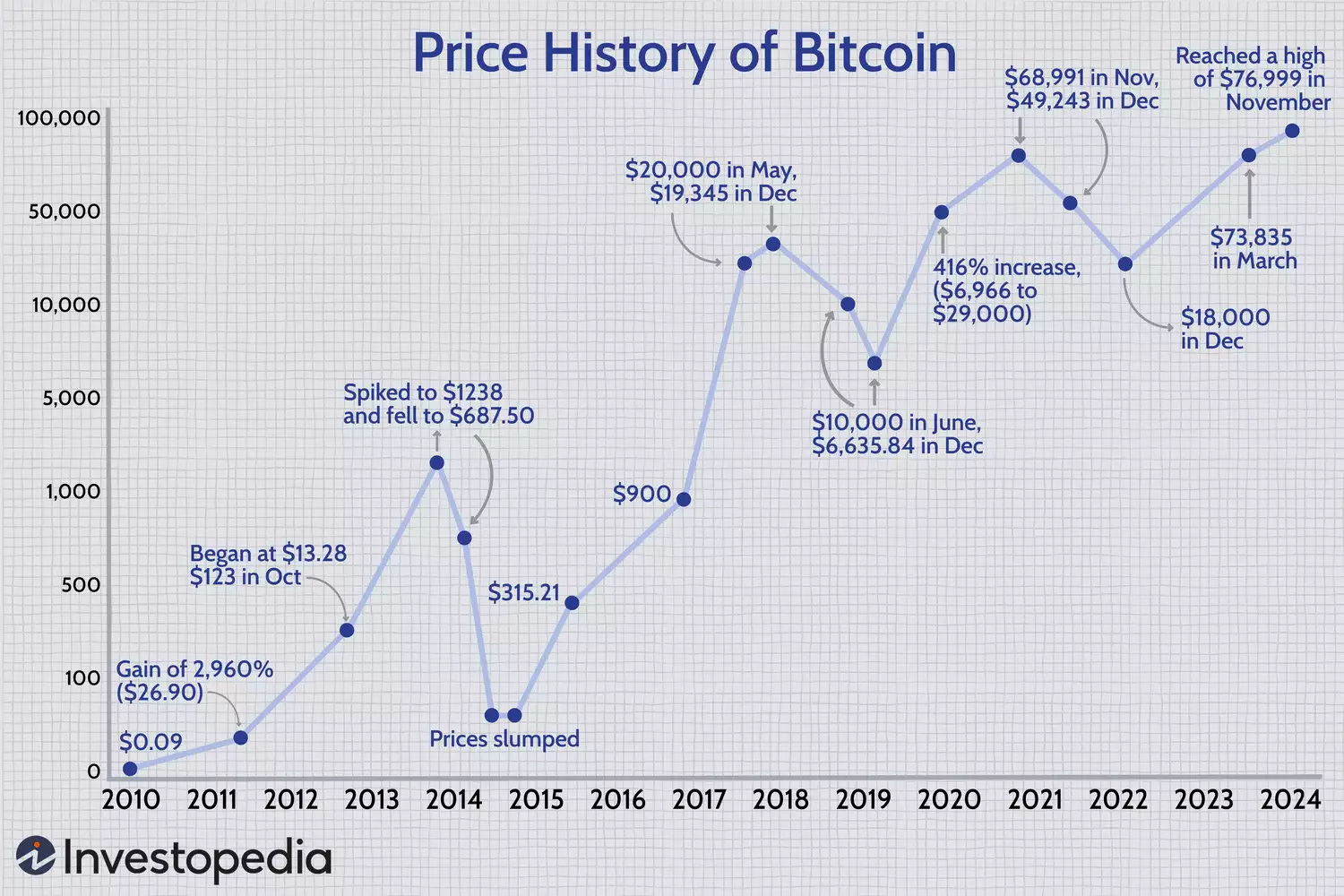

To judge effectiveness, it helps to look at real data. Bitcoin’s price since 2022 has swung wildly. For instance, by May 2022 it dipped under $30k and by December 2022 it was below $20k. Then in 2023–2024 it staged a massive rally: it opened 2023 around $16.5k and ended 2023 around $42k, then soared to roughly $100k by late 2024. Over such moves, what does DCA accomplish?

Example returns. The Nasdaq/Bitcoin Magazine analysis mentioned above shows one outcome: $10 per week for 5 years earned 202% return, versus only ~34% in gold or 23% in the Dow. Another case study (Medium article) simulated buying $100 monthly from Jan 2018 to Jul 2023; after spending $6,800 the investor held ~0.59 BTC worth about 61.9% gain by mid-2023. These examples illustrate that consistent investing in Bitcoin has often delivered strong growth, thanks to its long-term uptrend.

DCA vs. Lump-Sum in studies. Quantitative analysis shows differing conclusions. One crypto research report found that, over 2017–2023, lump‑sum investing typically accumulated more Bitcoin than DCA. For example, a 12‑month DCA plan acquired roughly 75% less BTC than investing all funds immediately. A related study noted that shorter‑interval DCA (e.g. weekly) narrowed the gap, but all DCA schedules underperformed lump-sum on average. In plain terms: if you have a fixed sum and Bitcoin keeps rising, you usually end up with more coins by investing it upfront.

Risk mitigation. On the other hand, some research emphasizes DCA’s risk benefits. An asset‑management study (Amdax) found that DCA “consistently lowers maximum drawdowns” compared to lump-sum, while “keeping overall performance equal”. In other words, DCA made the portfolio swings milder without sacrificing long-run returns. This confirms the classic view that DCA is essentially a risk-management strategy: it smooths out volatility at the cost of capping upside. For a cautious investor who can’t afford big drops, DCA may be “a suitable solution” to get exposure to Bitcoin without timing stress.

Conclusion

In summary, dollar‑cost averaging can be an effective way to accumulate Bitcoin if your goal is gradual, long-term investing with less stress about timing. It enforces discipline, often reduces the perceived cost of volatility, and protects against the worst case of buying everything right at a peak. For many newcomers or those building a position over time, these features are valuable.

However, DCA is not magic. If Bitcoin ultimately trends upward (as it has in recent years), putting your money in earlier rather than later tends to yield more Bitcoin. Data shows lump-sum investing often leads to higher accumulation when prices rise persistently, though it comes with sharper drawdowns. In other words, DCA is a trade-off: you give up some potential profit in exchange for steadier, less volatile growth.

Ultimately, the “best” strategy depends on your situation. If you have a lump sum and high risk tolerance, a one‑time purchase could outperform. If you prefer to average in over time and avoid FOMO, DCA can be very effective. As a Fidelity guide notes, DCA makes most sense when you believe Bitcoin will go up long-term and you want a simple, scheduled plan. Whichever method you choose, remain realistic: Bitcoin prices fluctuate dramatically (as they did from $16k to $100k in 2023–24), and no strategy can guarantee profits. DCA simply offers a structured, risk‑aware path to accumulate Bitcoin, with trade‑offs that each investor must weigh.

Sources: Financial educators and cryptocurrency analysts (Fidelity, Kraken, Coinbase, Investopedia) explain DCA’s general pros and cons. Recent market analyses and backtests provide Bitcoin‑specific results: e.g. a 5-year weekly DCA returned 202%nasdaq.com, while a study showed 12-month DCA gathered ~75% less BTC than lump-sum(with DCA reducing drawdowns). Historical price data is from Investopedia’s Bitcoin price chronology, reflecting Bitcoin’s 2022–2024 performance.